**This is not financial or legal advice** This information is for educational and entertainment purposes only.

Does your credit score feels like a mystery or a source of stress?

It can feel like you don’t have any control over the number and you probably aren’t even sure how it’s calculated.

It seems like a completely made up number and no one really knows exactly how it’s calculated.

Different companies give you different numbers, and it seems more like a social media secret algorithm than a real number that you can change.

Whether you’re aiming to buy a home, refinance, or just feel more financially confident, improving your credit score can open new doors.

The good news? You can raise your credit score 100 points in 6 months—and you don’t need perfect finances to do it.

In this post, I’ll walk you through simple, realistic steps to boost your credit score without the overwhelm. Let’s get started!

Why Your Credit Score Matters

Your credit score affects more than just loan approvals. It impacts:

- Interest rates on credit cards and loans

- Your ability to rent an apartment

- Insurance premiums

- Even some job opportunities

A higher credit score can save you thousands over your lifetime. So, improving it is a goal worth pursuing.

Having a higher score gives you more options and opportunities, so raising and maintaining your score, can impact your future self, more than you even realize.

How Your Score Is Calculated

Before we dive into raising your credit score, you have to know HOW it’s calculated in the first place.

Your credit score is calculated based on a couple main figures. But each company giving your score calculates it a bit differently, which is why your score can vary so much when you check it using different apps.

Your credit score is calculated based on several key factors in your credit history.

In the U.S., most lenders use FICO Scores or VantageScores, and while their formulas differ slightly, both consider similar components. Here’s how a typical FICO Score (the most widely used) breaks down:

1. Payment History (35%)

- Do you pay your bills on time?

- Late payments, collections, charge-offs, and bankruptcies negatively affect this part.

2. Amounts Owed (30%)

- Also called credit utilization.

- This measures how much of your available credit you’re using. Keeping balances below 30% of your credit limits helps your score.

- High balances relative to your limits can hurt your score, even if you pay on time.

3. Length of Credit History (15%)

- How long your credit accounts have been open.

- Older accounts and long-standing credit relationships improve your score.

4. Credit Mix (10%)

- Having a mix of credit types (credit cards, auto loans, mortgages, etc.) can help.

- You’re not penalized for lacking certain types, but variety shows you can manage different credit responsibly.

5. New Credit (10%)

- Recent applications for credit can lower your score temporarily.

- Multiple hard inquiries in a short period can signal risk.

| Factor | % Weight |

|---|---|

| Payment History | 35% |

| Amounts Owed | 30% |

| Length of Credit History | 15% |

| Credit Mix | 10% |

| New Credit | 10% |

Additional Notes:

- VantageScore uses similar factors but weighs them a bit differently and emphasizes recent behavior more.

- Checking your own credit (a soft inquiry) doesn’t hurt your score.

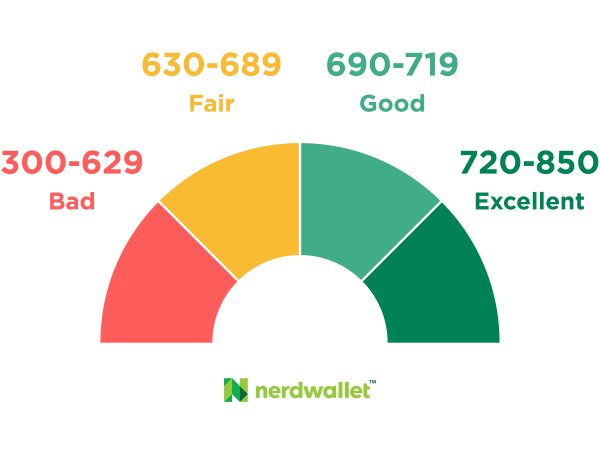

- Scores typically range from 300 to 850, with higher scores reflecting better creditworthiness.

How to Raise Your Credit Score 100 Points in 6 Months

Here’s a step-by-step roadmap to help you see real progress fast:

1. Check Your Credit Reports

Start by requesting your free credit reports from AnnualCreditReport.com.

Review for:

- Incorrect personal information

- Accounts you don’t recognize

- Payment history errors

Dispute any inaccuracies right away.

All agencies that are reporting on your report have to prove that it’s your debt. If they can’t prove it, they have to remove it.

Some people will dispute every single debt on their report, but in my opinion, that can be unethical if you know it’s your debt.

2. Pay Down Credit Card Balances

Credit utilization is one of the biggest factors in your score. Aim to keep balances below 30% of your credit limit, but ideally below 10%.

- Focus on paying down the smallest balances first

- Make small weekly payments if possible to lower your utilization faster.

Make sure and do the math to decide which balances to pay first. You want your balance to be less than 30% of your limit.

So, if you have a credit card with a limit of $30,000 limit, you’ll want the balance to be below $10,000.

3 Simple Steps to Pay Off Your Credit Cards

10 Easy Tips for Paying Off Debt FAST!

3. Make On-Time Payments Every Month

Your payment history accounts for 35% of your score. To build it:

- Set up automatic payments or calendar reminders.

- Pay at least the minimum on all accounts.

- Consider asking your creditors to move your due dates for better cash flow.

📌 You should also request that any debtors remove any late payments on your history.

The worst they can say is no! It doesn’t hurt to ask, especially if you are usually on time with payments.

4. Don’t Close Old Accounts

Length of credit history matters. Keep older, unused accounts open if they’re in good standing to help your score.

Now this is a smaller factor in your score, so if you need to remove the temptation by closing accounts, do it.

But try to keep the oldest ones open if you can.

Keep in mind that the accounts you close factor into the percentage of debt you have on your report.

Remember, you want to keep usage below 30%.

That usage percentage is for ALL your debts, not just each individual one.

So, if you close an account with a zero balance and a $5,000 limit, that will increase your overall usage percentage.

5. Request a Credit Limit Increase

Call your credit card company and ask for a credit limit increase—without a hard inquiry, if possible. This lowers your utilization without paying anything extra.

Remember that your utilization ratio is a huge part of your score.

So, asking to increase your limit will help with this without having to pay off a huge chunk of debt first.

The worst they can say is no!

It doesn’t hurt to call and ask.

6. Use a Credit-Builder Loan or Secured Credit Card

If your credit history is thin or you’re rebuilding after setbacks:

- Open a secured credit card

- Apply for a credit-builder loan from a credit union or online lender

Both help establish positive payment history.

Basically how a secure credit card works is that you put money on the card first, then that’s your limit. You can add to it and spend on it each month to help increase your credit score.

7. Avoid New Hard Inquiries

Each new loan or credit card application can temporarily drop your score. Be selective about applying for new credit during your six-month improvement window.

If you do decided to apply for new debt, make sure the inquires are within a short period of time, like 2 weeks to avoid bigger impacts on your score.

You can also request or ask if they can do a soft inquiry first.

They may not be able to, but some can.

8. Use Experian Boost or Similar Tools

Services like Experian Boost let you add utilities and streaming service payments to your credit file, helping raise your score if you have limited history.

This will help show on time payments and consistent payments as well.

It’s a small percentage of your overall score, but every little bit helps!

Can You Really Improve Your Credit Score 100 Points in 6 Months?

Yes! Especially if:

- Your current score is under 650

- You’re carrying credit card debt

- You’ve had missed payments, but are now current

By following these strategies consistently, many people see significant gains within six months.

Quick Recap: 6-Month Credit Score Action Plan

| Action Step | Why It Helps |

|---|---|

| Check and fix credit reports | Correct errors hurting your score |

| Lower credit card balances | Reduce utilization ratio |

| Pay on time, every time | Build positive payment history |

| Keep old accounts open | Improve credit age |

| Increase credit limits | Lower utilization instantly |

| Use credit-building tools | Establish or rebuild history |

| Avoid unnecessary applications | Prevent hard inquiry drops |

| Use Experian Boost | Add payment history to profile |

Final Thoughts

Raising your credit score isn’t about being perfect—it’s about being consistent. Start with small steps and track your progress.

Remember: every payment, every balance paid down, and every smart decision counts.

Ready to take control of your finances? Download my free Budget Blueprint to get started on your financial confidence journey!