If credit card debt has been weighing on your mind and wallet, you’re not alone—and you’re not stuck.

For many women over 40, credit card balances quietly pile up during years of caregiving, career shifts, emergencies, or simply trying to keep up. It’s easy to feel overwhelmed or even ashamed. But here’s the truth: you can take control of your credit card debt, one step at a time—and start feeling financially empowered again.

In this post, we’ll walk through seven practical, proven strategies that will help you pay off your credit card debt, stop the cycle of borrowing, and build lasting momentum. Whether you’re just getting started or need a plan that finally sticks, this is for you.

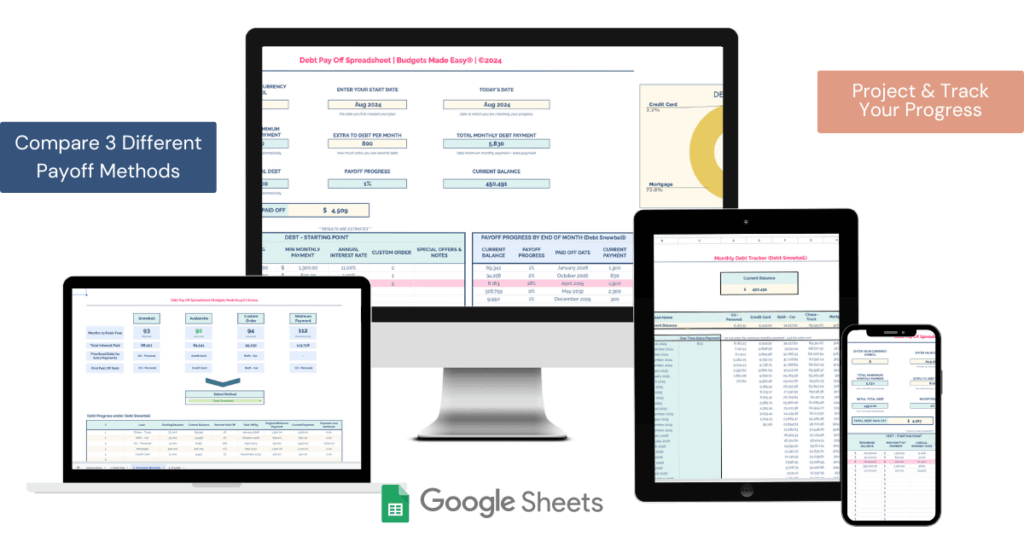

🔥 While you are here grab your Debt Pay Off Spreadsheet – Just $9! 😎

Quickly and easily compare different pay off methods, including picking your own order. Project future balances on specific dates AND track your progress each month.

1. Get Clear on Your Debt Picture

You can’t change what you’re not willing to look at—so the first step is facing your numbers.

This is the hardest part for most people because it’s easier to avoid it than to look at it.

I get it.

But you can’t start taking action if you don’t know what you are dealing with.

Ideally, I want you to make a list of every credit card you carry:

- Name of the card

- Total balance

- Interest rate (APR)

- Minimum monthly payment

Seeing it all laid out in one place can feel scary, but it’s also empowering. This is your starting point—not your forever.

If that feels too scare, then just pick one or two credit cards to start with.

Try this:

Use a simple spreadsheet or debt tracker to stay organized. If you’re more visual, color-code balances or use a printable debt thermometer to track progress.

💬 Reflection prompt: How does your debt currently make you feel—and how would you like to feel about your money six months from now?

2. Stop Adding New Debt

Paying off credit cards while still using them is like trying put out a fire, while lighting more fires behind you.

Pause credit card use while you focus on your payoff plan.

This means:

- Using debit or cash for everyday spending

- Removing cards from your wallet or phone

- Unsubscribing from tempting promo emails and alerts

✨ Even if you get reward points. It’s more important to get your spending under control than worry about pennies on the dollar in rewards.

Look at your recent statements to spot patterns: Are certain purchases triggering overspending? Knowing your spending habits helps you stay in control.

Your money habits are the foundation to your success!

3. Choose a Repayment Strategy That Fits Your Style

There’s no one “right” way to pay off debt—the method you stick to is the one that works best.

Here are the three best approaches:

👉 Debt Snowball:

Pay off your smallest balance first while making minimum payments on the rest. Once that’s gone, roll that payment into the next-smallest debt.

✨Great for motivation and quick wins.

👉 Debt Avalanche:

Focus on the card with the highest interest rate first, regardless of balance. You’ll save the most money in the long run.

✨ Best if you’re motivated by numbers and long-term savings.

👉 Impact Method™:

Focus on the debt that will have the biggest impact on your life.

That could be in your budget, so the payment amount OR it could be emotional.

✨ Focuses on giving you a big reward quickly.

Need help choosing?

If you love checking boxes and fast wins, go Snowball.

If you want to maximize your savings and don’t mind a slower start, Avalanche might be your fit.

But it’s important to run the numbers and actually compare the numbers.

It’s also okay to change your approach over time. Just because you pick one doesn’t mean you can’t change it later.

✨ Remember, the best method is the one you follow through with! ✨

Check out the Debt Pay Off Spreadsheet to compare the methods!

Quickly see when you can be debt free or just certain debts and project what your balances will be in the future.

Plus track your progress as you go and watch your balances drop each month!

4. Cut Costs and Free Up Cash

Once you have a plan, you need to take action on it.

Start by scanning your budget for “money leaks”:

{kind=link}

- Streaming services you rarely use

- Frequent dining out

- Subscription boxes or memberships on autopilot

Even $50–$100 a month can make a big difference when applied to debt consistently.

Challenge yourself:

This week, find $100 in your budget to apply toward your highest-priority credit card. Then do it again next week.

Or try a No Spend Challenge.

{kind=link}

5. Reduce Your Interest Rates

The less interest you pay, the faster you can become debt-free.

Here are three options to explore:

✅ Call Your Credit Card Company

Ask if they’ll lower your APR. It’s a simple call that can work—especially if you’ve been a long-time customer.

They will often work with you and give you offers—even if you aren’t behind on payments. It never hurts to call and ask!

✅ Balance Transfer Credit Card

Some cards offer 0% interest for 12–18 months.

Just be sure to:

- Read the fine print

- Pay it off before the promo ends

- Avoid adding new purchases to the card

- Do the math to see if the transfer fee makes sense

✅ Debt Consolidation Loan

Rolling multiple cards into one loan with a lower interest rate might simplify payments—but be careful. Only pursue this if you have a solid plan and won’t rack up more debt afterward.

6. Set Up Automatic Payments and Track Progress

Setting up autopay can help you stay on track and avoid late fees. If possible, automate more than the minimum to accelerate your payoff.

Visual progress tools—like a debt tracker, calendar reminders, or payoff chart—keep you focused and motivated.

Bonus Tip: Create a weekly “money check-in” routine. Review balances, celebrate small wins, and stay connected to your goals.

{kind=link}

7. Celebrate Small Wins Along the Way

Don’t wait until you’ve paid everything off to feel proud. Every step forward is a win worth recognizing.

Ideas for non-spending celebrations:

- Light a candle and write a gratitude note to your future self

- Take a nature walk and reflect on your progress

- Create a “victory jar” and drop in a note each time you pay off $100

Momentum builds when you stay encouraged.

Bonus Tip: Get Support and Accountability

You don’t have to do this alone. Whether it’s a trusted friend, a money coach, or a supportive online group, having someone to check in with can boost your confidence and consistency.

Final Thoughts: You’ve Got This

Paying off credit card debt isn’t just about the math—it’s about rewriting your money story. Every payment you make is proof that you’re taking control, making empowered choices, and building a future that feels lighter.

Start today by choosing just one step from this list. Even a small action—like reviewing your interest rates or setting up a payment tracker—can lead to big change over time.

✨ You are capable. You are worthy. And it’s never too late to take control of your money.

🔥 Grab your Debt Pay Off Spreadsheet – Just $9! 😎

Quickly and easily compare different pay off methods, including picking your own order. Project future balances on specific dates AND track your progress each month.