If you want to live a successful retirement, it’s important to get your finances in order. Don’t procrastinate on outlining financial goals and a budget.

The faster you can get your finances in order, the more efficient you will be at saving for retirement and building your ideal life.

For some retirement savings and money management tips, check out our guide below.

Outline a Spending Plan

While it’s easier to get away without having a spending plan when you’re young and have more income streams, it’s more important to get organized as you’re older. This is because you likely won’t be receiving as much money in retirement as you were when you were working.

If you aren’t already in retirement, figure out what your monthly expenses typically are. How much of your funds are going toward necessities like housing and health care and how much are you spending on luxuries like traveling, going out to eat or spending money on clothes?

Once you figure out how much you’re spending each month, think about how your expenses are going to change in retirement. Check out our article about common budgeting mistakes to help inform your spending plan.

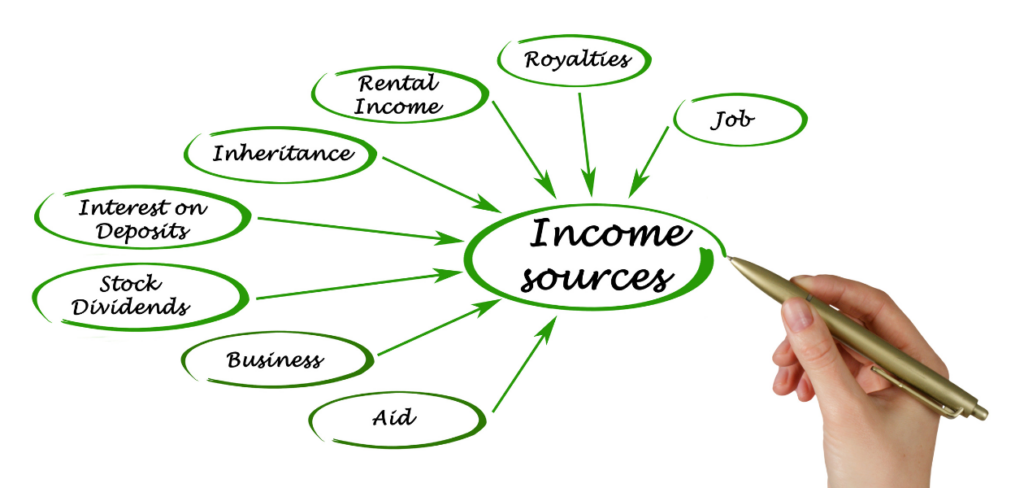

Add Your Income Streams

Think about where you’re going to be receiving money from during retirement. Have you delayed your Social Security payments? Are you going to be living off of the money you’ve saved in your 401(k) or IRA? Or are you planning to work during retirement?

Wherever your income is coming from, make sure to write it down. Then you can add together what your monthly income is looking like and work backwards from there. As you do so, visualize your ideal retirement. Do you want funds that you can put toward traveling or moving to a place with a higher cost of living? If that’s the case, try to factor those luxuries into your budget.

That said, if you don’t have enough money, you may want to consider looking at alternative income sources or rethink your savings strategy.

Build an Emergency Fund

Emergency funds are important for everyone, but even more so for retirees. Since you have less income coming in, it can do more damage to your savings when emergency expenses arise. This is why you should be setting aside a certain amount of money each month toward building an emergency fund.

Here are some tips for setting up a successful emergency fund:

- Start small: As you start saving, you don’t want to stress yourself out. Start with small, monthly contributions to a savings account and then you can build up these contributions as you see fit.

- Automate savings: If you have to manually contribute savings to your emergency fund every month, it’s easy to forget to do so all together. Most banking apps allow you to automate monthly contributions. This helps take the pressure off and gives you one less thing to worry about.

- Monitor your progress: Make sure to check in on your savings regularly to ensure you’re making adequate progress. If you feel you aren’t saving enough, it could be time to increase your monthly contributions if possible.

Using the above strategies, you’ll be sure to have a sizable emergency fund in no time. That way, you aren’t feeling a background anxiety about a possible financial crisis arising.

Diversify Your Savings

When it comes to investing, you don’t want to put all of your eggs in one basket. It’s smart to allocate your money toward different assets to reduce your overall risk.

For example, if you put all of your money into a single stock, it’s possible for that stock to plummet, resulting in you losing most or all of your money. When you invest in several different stocks, however, it becomes less likely that that will happen.

The three primary asset classes you can invest in are bonds, stocks and cash alternatives. You can also invest in resources like gold and coal or in real estate. Bonds are typically more safe than stocks, but yields less money. Stocks have the potential to yield higher returns, but at a greater risk of losing money.

When you’re younger, you typically have more risk tolerance. You can make riskier investments that may yield higher rewards, since you have more time to save money before retirement.

As you get older, however, you’ll want to play it more safe with your investments since you’ll need your savings for an upcoming retirement.

Try to diversify your investments across asset classes according to your risk tolerance.

Communicate With Your Partner

If you’re planning to retire with a partner, it’s important to communicate about your current financial situation and overall financial goals. Make retirement planning a shared priority between the two of you to ensure that you are each headed toward a retirement you’re satisfied with.

You may want to consider scheduling one time or a couple of times a month to discuss the state of your finances. Does one of you have student loan debt or credit card debt? These could be the first things that you prioritize to pay off.

Consider whether you should combine bank accounts or keep your funds separate. There is no right or wrong way to manage your finances together. Find which solutions work best for you and communicate along the way.

Most of all, both of you need to make sure not to keep money secrets from the other. It’s important that when you plan a vision for the future together, you know everything about each other’s finances. This makes it easier to coordinate savings and reach your financial goals.

Prioritize the Essentials

Before you start thinking about your dream retirement vacation, outline what essentials need to be paid for first. On average, retirees spend most of their budget on health care, housing, transportation and food expenses. Once you’ve gotten the essentials out of the way, you can worry about budgeting for nonessential items like going on a vacation.

If you’re having trouble cutting back on your spending, check out our article about ways to trim unnecessary spending habits.

Consider Moving

While moving costs money, it can also save you money in the long run. For example, you might look for states that don’t tax social security or states with a lower cost of living. You could also find cities with great public transit options so you can save money on transportation.

When you move, it could also improve your quality of life over all. Just be sure to do ample research before you start packing your things and moving.

It’s a big decision to move, particularly when it’s far away from your family or other loved ones.

To save money on moving, you may want to wait until the winter, since moving season peaks during the summer.

Consider Delaying Social Security

For every year you delay your Social Security check, your benefits increase by 8% for the subsequent year. So if you can afford to delay your check, it could be a way to earn extra money down the road.

If you change your mind and realize that you need your Social Security check after delaying, there shouldn’t be an issue. You can choose to start claiming your check whenever you want after you reach your full retirement age.

Find a Roommate

While retirees don’t typically think about finding a roommate as an option, it’s a totally feasible way to save money. If you don’t have a partner in retirement, having a roommate is a great way to acquire companionship and a lower cost of living.

Just make sure that you have a roommate that you get along with. Additionally, it’s important that you can communicate with them about difficult issues.

After all, the last thing you want is a roommate that can’t take care of their share of the housework.

Research Debt Payment Options

As a senior, you’re likely to experience higher health care costs as your risk of illness increases with age.

This can lead to high levels of debt which, when left unchecked, could lead to bankruptcy. And health care costs aren’t the only source of debt seniors experience.

You might hold debt from credit cards, mortgages, or even student loans. To avoid letting this debt hover over you in retirement, it’s a good idea to look into forgiveness options to make it more manageable.

Here are some debt forgiveness options you can explore:

- Debt consolidation: Get a debt consolidation loan to pay off your other sources of debt so that you have less lenders you need to keep track of. This will help you keep your payments organized and, if your consolidation loan has a lower interest rate than your initial loans, it could save you money in the long run.

- Negotiate a settlement: If you find your debt over 90 days overdue, it’s possible to negotiate a debt settlement. Either contact your lender yourself or connect with a debt settlement company. The process takes time and effort, but can substantially reduce the debt you owe.

- Write a financial hardship letter: If you find yourself in deep medical debt, it’s sometimes possible to negotiate a lower debt by sending a letter outlining your financial situation. While your creditor might refuse your request, the worst they can say is “no.”

Debt isn’t an easy thing to deal with when it accumulates. Whenever you take out a loan or collect any types of debt, make sure you have a plan in place to pay it off. When you allow it to build, it could lead to disastrous consequences on your credit and overall financial situation.

Create Specific Financial Goals

If you don’t have specific financial goals, it can be difficult to find the motivation to save money in the first place. To start, just list out every possible goal related to finances that comes to your mind. You might list things such as:

- Paying off all of your debts

- Owning your own home

- Improving your credit score

- Buying a vacation home

- Buying a Tesla

Regardless of how far fetched your goals are, list them onto paper or in a Google Doc. Once you feel satisfied with your list, it’s time to get a bit more realistic.

Now you should rearrange your goals by priority. For example, buying a Tesla would likely go more toward the bottom of your list if you need to pay off student loans or mortgage payments.

Once you have a clear picture of where you want your funds to go, it will become easier to abide by your budget. Try to make sure that each of your goals aligns with a larger motivation in your life. Think about what the purpose is behind each of your goals.

Conclusion

While retirement saving is simple, it isn’t always easy. If you aren’t used to abiding by a budget and putting aside funds for specific financial goals, it can take some getting used to. That’s why it’s important not to overwhelm yourself. Don’t try to implement all of the above tips at once. Instead, improve your financial situation one step at a time. In the long run, you’ll find yourself more financially stable and headed toward a nice retirement.

If you need help organizing a retirement budget, check out the retirement budgeting worksheet below.

This post is a guest post from Retire Guide. Check out the full guide here.